Dillan Dove - Information Effect Project

Debt and Financial Literacy, or the Lack Thereof

The word “epidemic” according to Merriam-Webster’s dictionary is defined as, “affecting or tending to affect a disproportionately large number of individuals within a population, community, or region at the same time.” Often when we hear the word “epidemic” we tend to think of mass viruses or types of sicknesses that spread and are on the verge of spreading. We fear said sicknesses and viruses but many times think, “That could never happen to me or us.” There is an epidemic that has and continues to hurt and affect those ones we love along with countless others more and more; debt and financial literacy or the lack thereof.

Debt, what is it?

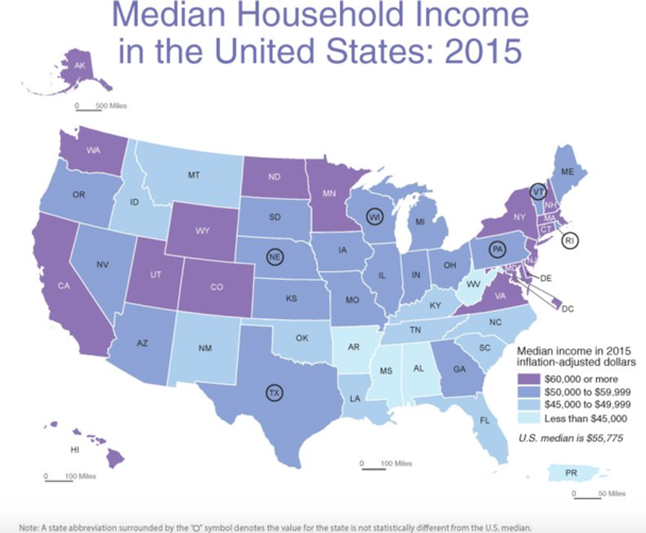

Debt it is the state of owing something or someone. In the “2015 American Household Credit Card Debt Study” they found that the average American household with exception of debt accrued from mortgages is well over $120,000. (Johnson) Add in a mortgage and you are looking at close to $300,000 or more. The average American household income according to the ACS Census in 2015 was $55,775 per year which is a 3.83% increase from the year prior. (Numbers) It would take more than 20 years on said income to be able to pay off this amount of debt. In the image below, we can see the median household income in 2015. The shocking point here, only about 15 of our 50 states’ median household income is above the national average.

The word “epidemic” according to Merriam-Webster’s dictionary is defined as, “affecting or tending to affect a disproportionately large number of individuals within a population, community, or region at the same time.” Often when we hear the word “epidemic” we tend to think of mass viruses or types of sicknesses that spread and are on the verge of spreading. We fear said sicknesses and viruses but many times think, “That could never happen to me or us.” There is an epidemic that has and continues to hurt and affect those ones we love along with countless others more and more; debt and financial literacy or the lack thereof.

Debt, what is it?

Debt it is the state of owing something or someone. In the “2015 American Household Credit Card Debt Study” they found that the average American household with exception of debt accrued from mortgages is well over $120,000. (Johnson) Add in a mortgage and you are looking at close to $300,000 or more. The average American household income according to the ACS Census in 2015 was $55,775 per year which is a 3.83% increase from the year prior. (Numbers) It would take more than 20 years on said income to be able to pay off this amount of debt. In the image below, we can see the median household income in 2015. The shocking point here, only about 15 of our 50 states’ median household income is above the national average.

It doesn’t stop here

As disturbing as it is to see over 70% of our great nation at or below the national average income per household, the real issue lies in the aftermath of this epidemic we call debt. Sadly, the majority of families will never see an end to the debt in their lifetime and in most cases, their children may not either. In a new study done by Pew Charitable Trusts, they found shocking statistics that strike not only your nerve, but also the nerve of those born in the early 1900’s.

As disturbing as it is to see over 70% of our great nation at or below the national average income per household, the real issue lies in the aftermath of this epidemic we call debt. Sadly, the majority of families will never see an end to the debt in their lifetime and in most cases, their children may not either. In a new study done by Pew Charitable Trusts, they found shocking statistics that strike not only your nerve, but also the nerve of those born in the early 1900’s.

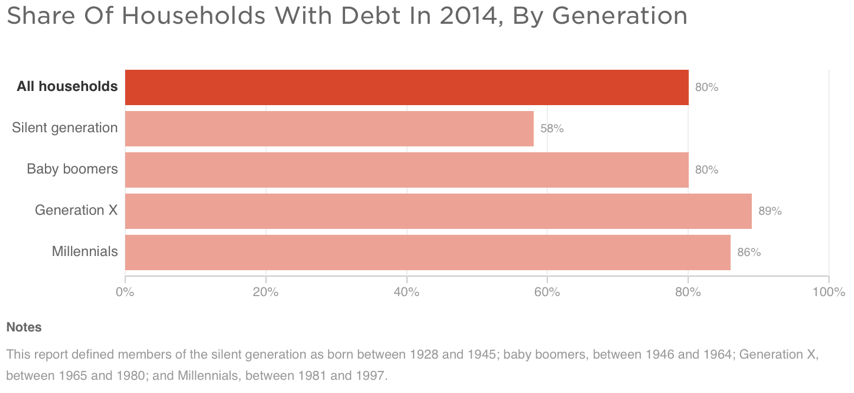

We can learn a lot from the graph shown above. We start out by seeing that about 80% of ALL households have some sort of debt. Then, by generation we see how many households of these continue to have debt. What is most alarming detail here, the “silent generation”, where more than 90% of this generation are retired, more than half carry some sort of debt to this day (Noguchi). Thus indicating that debt, distinctive to a paycheck, does not merely end but carries on through each generation.

Now what?

So what now? Are we out of luck? What are we doing to correct this problem that so many people are facing? Sadly, a lot of people simply feel that we should just leave finance and economics to the experts and move on. Think back to your late childhood, junior high and high school. Do you remember learning anything about finance, taxes, debt or even money in general? I’m sure you remember at least learning something about the cells or some other scientific term and leaves right? That should help you in the future as you start to pay bills. Could this be where the real issue lies?

The real problem

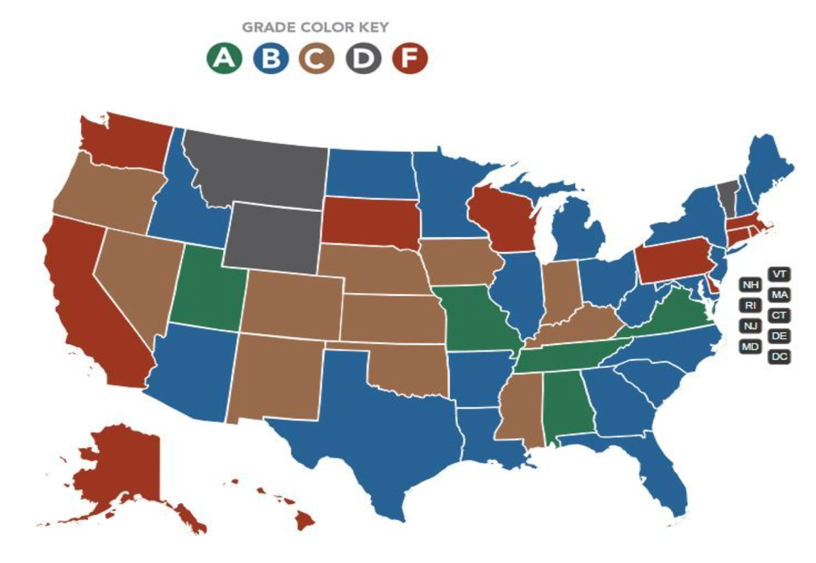

In 2013 a study conducted by the National Foundation for Credit Counseling, “40% of adults would grade themselves a C, D, or F for their knowledge of personal finance. Nearly one-third of adults reported that they have no savings, according to the same study.” Again, thinking back to the school years, “C” is average, “D” is below average, and “F” is failing. That is letting us know that close to half of the countries adults are average to failing when it comes to money in general. (Goodkind) This could very well explain the issue of debt that has swept and continues to sweep our nation. In the image below, only FIVE of the 50 states would have given themselves with an “A” grade.

Now what?

So what now? Are we out of luck? What are we doing to correct this problem that so many people are facing? Sadly, a lot of people simply feel that we should just leave finance and economics to the experts and move on. Think back to your late childhood, junior high and high school. Do you remember learning anything about finance, taxes, debt or even money in general? I’m sure you remember at least learning something about the cells or some other scientific term and leaves right? That should help you in the future as you start to pay bills. Could this be where the real issue lies?

The real problem

In 2013 a study conducted by the National Foundation for Credit Counseling, “40% of adults would grade themselves a C, D, or F for their knowledge of personal finance. Nearly one-third of adults reported that they have no savings, according to the same study.” Again, thinking back to the school years, “C” is average, “D” is below average, and “F” is failing. That is letting us know that close to half of the countries adults are average to failing when it comes to money in general. (Goodkind) This could very well explain the issue of debt that has swept and continues to sweep our nation. In the image below, only FIVE of the 50 states would have given themselves with an “A” grade.

Why is this not a subject focused on in schools? This is something people actually DO use on an everyday basis. Financial expert Annamaria Lusardi, professor of economics and accountancy at the George Washington University School of Business and academic director at the Global Financial Literacy Excellence Center, had a lot to say in a discussion with U.S. News and World Report. “The United States has one of the most developed financial markets in the world, and ‘a country with the most developed financial markets should not be average, given the decisions young people are already asked to make,’” She explained as she talked about large loans and debts they have taken on.

The solution?

Lusardi luckily had some ideas for solutions to the issue she shared. “For this generation, I don’t think there is any solution other than putting financial literacy in schools,” Lusardi says. Just as students learn math and English, they should learn financial literacy because it is also a basic skill that young people need, she argues. She later mentioned that perhaps financial literacy is something that should be taught earlier than at the high school level. “What if when young people started their first job, they already [knew to] put money into their retirement account? If young people could do this at age 20 rather than age 50, it would make an enormous difference,” (Palmer).

Now is the time to ACT

It doesn’t take years of school or any special knowledge or degree to recognize the problem at hand. In one way or another we are all affected by debt and the lack of financial literacy. So, what can YOU do to make a change? You can petition for your local schools to add financial education to the everyday curriculum. If together we unite and recognize the issue we can make a difference. There are also so many things we can do close to home to help those immediately around us. We can teach our children in home the importance of money, saving, preparation for the future, and hard work. We can study and research things for ourselves to prepare for our own futures. There are online courses we can take and invest in ourselves for a change. The resources really are limitless.

The most important part is that we ACT. Just how you forgot how many cells are in a leaf or the axis of similitude of three circles, if you do not act on this, you too will continue to follow the long and never ending spiral of debt and financial negligence.

Now it is YOUR turn. What will you do?

The solution?

Lusardi luckily had some ideas for solutions to the issue she shared. “For this generation, I don’t think there is any solution other than putting financial literacy in schools,” Lusardi says. Just as students learn math and English, they should learn financial literacy because it is also a basic skill that young people need, she argues. She later mentioned that perhaps financial literacy is something that should be taught earlier than at the high school level. “What if when young people started their first job, they already [knew to] put money into their retirement account? If young people could do this at age 20 rather than age 50, it would make an enormous difference,” (Palmer).

Now is the time to ACT

It doesn’t take years of school or any special knowledge or degree to recognize the problem at hand. In one way or another we are all affected by debt and the lack of financial literacy. So, what can YOU do to make a change? You can petition for your local schools to add financial education to the everyday curriculum. If together we unite and recognize the issue we can make a difference. There are also so many things we can do close to home to help those immediately around us. We can teach our children in home the importance of money, saving, preparation for the future, and hard work. We can study and research things for ourselves to prepare for our own futures. There are online courses we can take and invest in ourselves for a change. The resources really are limitless.

The most important part is that we ACT. Just how you forgot how many cells are in a leaf or the axis of similitude of three circles, if you do not act on this, you too will continue to follow the long and never ending spiral of debt and financial negligence.

Now it is YOUR turn. What will you do?